A normal mortgage generally demands a credit history away from 640 or highest. Into an incident by the case basis, score anywhere between 620-639 is also qualify with regards to the level of assets the newest debtor features.

FHA Financing Credit score:

Minimum credit history needed for FHA is an effective 620. Once more, towards an incident by circumstances base scores ranging from 580-6ount from property, and you may debt proportion the fresh new debtor keeps.

The utmost financial obligation-to-earnings ratio to have a normal Loan was forty five%. It indicates your monthly debts (including the mortgage payment) do not meet or exceed 45% of revenues. We have risen to an excellent 50% personal debt ratio, although individuals had extremely high results and you can a large amount off possessions.

FHA Mortgage Loans in order to Income Ratio:

FHA are easy as compared to Traditional. Maximum debt-to-earnings ratio to possess a keen FHA financing are fifty%. We’ve got got borrower wade all the way to 55%. Large financial obligation-to-income ratios would wanted compensating items, which would feel credit score, or many assets.

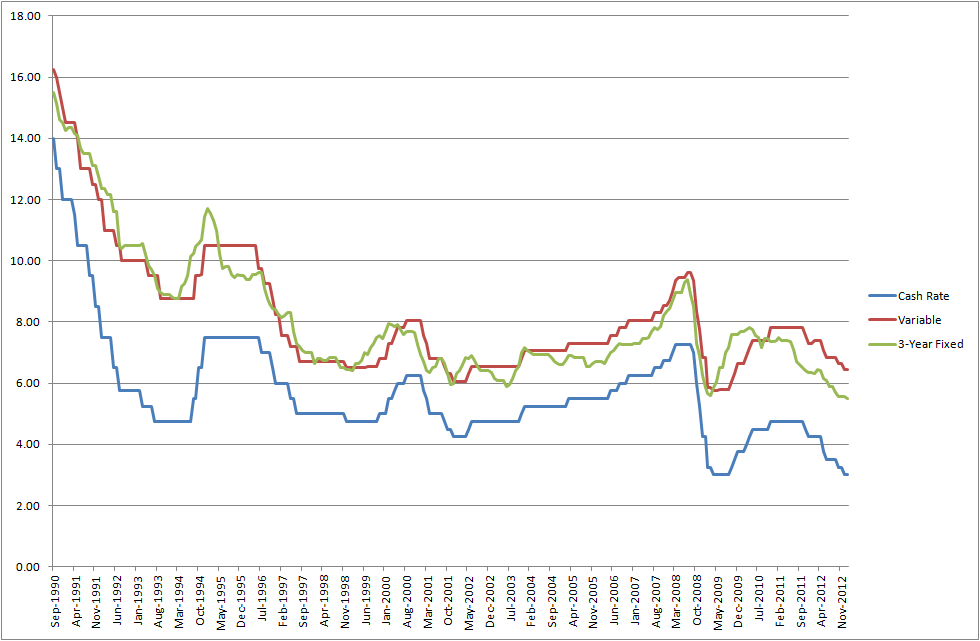

Interest rates on a conventional are generally higher than FHA

The eye rates on a traditional Mortgage are greater than the interest prices on the an FHA mortgage, Although traditional mortgage doesn’t require homeowners insurance otherwise possessions fees are within the month-to-month homeloan payment.

Whilst price is highest, you don’t have to spend the money for resource payment of just one.75% in addition to month-to-month PMI is generally less than FHA. Pose a question to your financing officer to-break down the different alternatives getting you.

The speed is not always large, if you have fantastic borrowing, it may be less than the new FHA rate of interest.

FHA Mortgage Interest rates:

FHA was an effective governent program and you will usually has straight down rates of interest than simply Old-fashioned. FHA do need to have the assets taxation while the home insurance to help you be added to new payment per month. The new PMI can be highest for the FHA than simply Antique.

Traditional financing don’t require repairs

Inside the a retailers field, when there are multiple even offers into a home, the vendor may like a buyer who’s bringing a conventional loan unlike FHA.

FHA needs services meet up with the requirements away from safety. An enthusiastic appraiser will make sure the house you get satisfy such conditions.

Its faster works and cash to your seller to go with a buyer that is having fun with a normal mortgage rather than FHA, simply because they don’t need to value resolve requirements.

Whether your home is in the great condition, then provider may go that have an enthusiastic FHA buyer. It really hinges on the house or property while offering that seller gets.

Refinancing is a lot easier that have a keen FHA financing

For individuals who actually have an enthusiastic FHA financing, and want to refinance when deciding to take benefit of a lower life expectancy rates it is easier to re-finance that have FHA.

FHA features a loan known as FHA streamline, the mortgage doesn’t require an appraisal or income data. It’s quick and easy.

Traditional will demand an assessment and you may money data files. Individuals should make certain that they meet the obligations-ratio assistance plus the assessment will WI installment loans direct lenders have to have been in in the worthy of.

Conventional doesn’t require condo acceptance eg FHA.

In the event that to buy a flat, it needs to be FHA accepted when the playing with a keen FHA mortgage. Conventional doesn’t have so it specifications.

Traditional against FHA Summary

- Have higher credit standards. Cannot make it credit imperfections.

- Financial obligation in order to money ratios was more strict

- PMI can be removed at 80% financing in order to worthy of

- Refinances want money docs and appraisals

- Allowed to purchase funding qualities

- Keeps down payments as low as step three%

- Should buy condos

- Permitted to waive property income tax and home insurance out-of payment per month